/Goldman Says: Central Banks Will Be Buying Gold for 3 More Years

Goldman Says: Central Banks Will Be Buying Gold for 3 More Years

By Scottsdale Mint

on

Bottom Lines

Gold has broken out of its consolidation range, supported by ETF inflows, speculative positioning, and renewed central bank demand.

Risks to the $4,000/toz mid-2026 forecast lean upward, though short-term pullbacks remain possible due to speculative positioning.

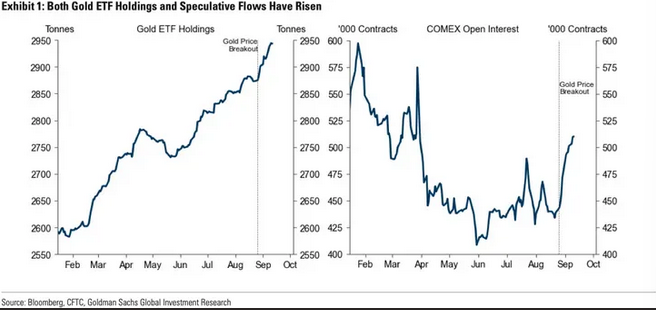

Gold’s Breakout and Drivers

Gold has pushed above its multi-month consolidation range of $3,200–3,450 per ounce, gaining 6 percent since August 26 to reach about $3,650. According to Goldman analysts Lina Thomas and Daan Struyven, the breakout reflects the influence of three key buyer groups:

ETFs,

speculative funds,

and central banks resuming purchases after the summer pause.

Now they update clients currently in this latest report:

“Rising ETF holdings contributed about 1.5 percentage points to the 6 percent rally, stronger speculative positioning added around 1.2 points, and likely central bank demand did the rest.”

This combination provided the push required for prices to move out of their range-bound condition.

Goldman maintains for now its mid-2026 forecast of $4,000 per ounce. The forecast is underpinned by structural central bank demand and the likelihood of steady ETF inflows. A supportive backdrop includes Federal Reserve easing and the 30 percent probability of a U.S. recession over the coming year, both of which could amplify safe-haven flows.

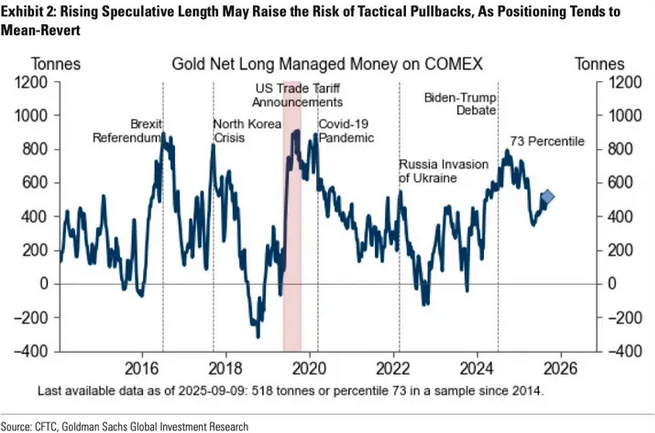

Positioning Risks and Tactical Pullbacks

While the bank remains constructive on the longer-term outlook, it acknowledges short-term risks. Futures markets reveal a notable rise in speculative length, which tends to revert toward more neutral levels. The analysts caution, “while we see the risks to our $4,000 mid-2026 forecast as skewed to the upside, rising speculative length raises the risk of short-term corrections.”

This points to the possibility of near-term setbacks, even as the overall trajectory continues to favor higher levels.

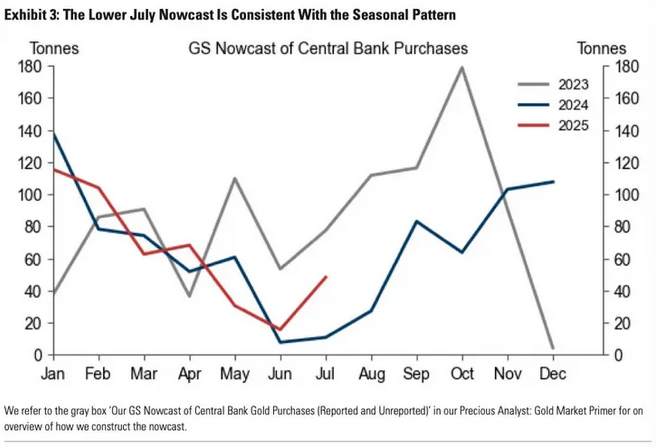

The Seasonal Central Bank Lull

The July nowcast for central bank and institutional demand on the London OTC market came in at 48 tonnes, well below the 2025 monthly forecast of 80 tonnes. Goldman emphasizes that this shortfall is in line with a well-documented pattern. “Central bank purchases tend to slow in the summer and re-accelerate from September.”

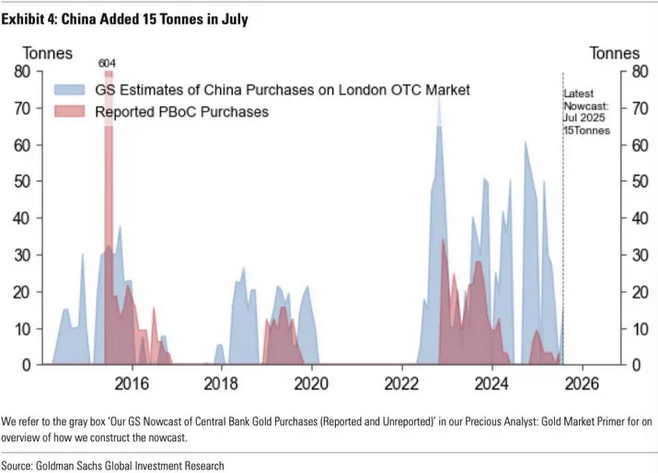

Year-to-date flows average 64 tonnes per month, modestly below forecast. However, the analysts stress that the seasonal dip does not undermine the broader outlook. Qatar led July purchases with 20 tonnes, while China followed with 15 tonnes. These figures demonstrate the continued leadership of emerging market buyers.

A Three-Year Horizon for Official Demand

Goldman frames current buying in the context of a structural change in reserve management that began after 2022. The freezing of Russian reserves spurred central banks, particularly in emerging markets, to diversify more aggressively. “We view this as a structural shift in reserve management behavior, and we do not expect a near-term reversal,” the analysts note.

The bank’s base case assumes this elevated demand continues for at least three years. The logic rests on the large gap between emerging market allocations and those of developed markets. China currently holds only 8 percent of reserves in gold, compared with roughly 70 percent in the United States, Germany, France, and Italy. The global average is about 20 percent, which Goldman identifies as a reasonable medium-term target.

Russia provides a precedent, having raised its gold share from 8 percent to 20 percent between 2014 and 2020 while repatriating reserves before sanctions. Goldman sees China on a similar path.

China’s Path Toward 20 Percent

If the largest official buyer-China -were targeting an allocation of 20%, and maintained an average pace of ~40 tonnes per month4 (in line with recent patterns), we estimate it would take approximately three years to reach a 20% gold share.

If China were to target 20 percent, maintaining purchases of 40 tonnes per month, the goal could be reached in about three years. Higher prices would accelerate the process by lifting the value of existing holdings, thereby reducing the volume of new purchases required. As the analysts put it, “sustained global central bank buying would likely raise gold prices over time, thereby increasing the notional value of existing holdings and helping reach allocation targets more quickly.”

This calculation underscores the reinforcing loop between central bank accumulation and higher market prices.

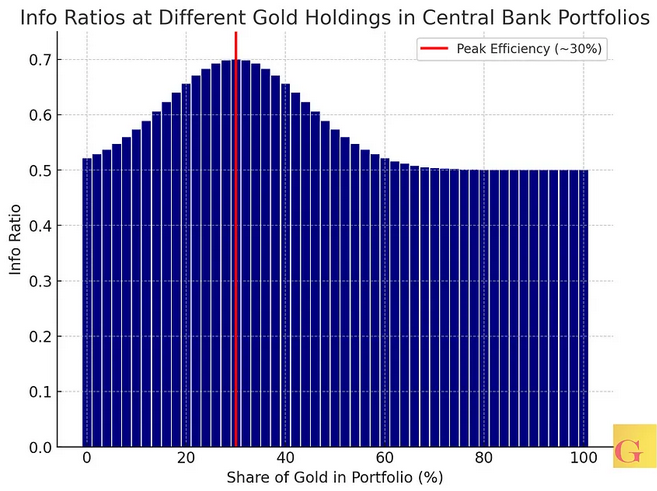

Bank of America Believes 30% is Most Efficient

Note Bank of America also thinks 20% is the current level, but 30% will be the new level for proper diversification. Poland recently raised its target level to 30%. Bank of America argues that central bank portfolios are most “efficient” when gold accounts for roughly 30% of reserve assets. At present, the share of gold in reported reserves in our research sits closer to 20%, up from about 11% two decades ago. This rise reflects the steady accumulation of bullion by central banks, a trend highlighted by the World Gold Council and IMF statistics.

The blue bars trace the “efficiency” of portfolios at varying gold allocations. The red vertical line at 30% marks the point where info ratios peak, illustrating the optimization level BofA suggests. The question then, is straightforward: how much more gold would central banks need to buy to move from today’s 20% to the suggested 30%?

Goldman is not suggesting central banks are going to raise their allocations to 30%.. not yet anyway.

Survey Evidence Confirms the Shift

The World Gold Council survey provides further confirmation. Ninety-five percent of central banks now expect global gold holdings to rise in the next 12 months, up from 81 percent in 2024. None expect a decrease. Forty-three percent plan to increase their own holdings, compared with 29 percent a year ago, and none plan a reduction.

This evidence highlights the durability of official demand and its growing importance in shaping the global gold market.

Conclusion

Goldman interprets the recent breakout as a reflection of renewed strength across ETFs, speculative funds, and official buyers. Seasonal weakness aside, the structural shift in central bank behavior is expected to continue for several years, with China’s underweight position offering a clear roadmap for further accumulation.

The $4,000 per ounce forecast for mid-2026 stands, with the bias toward higher outcomes. Short-term corrections remain possible, but the foundation of central bank and ETF demand suggests that the rally rests on durable support.

About the Author

Vincent Lanci is a commodity trader, Professor of MBA Finance (adj.) , and publisher of theGoldFixnewsletter.