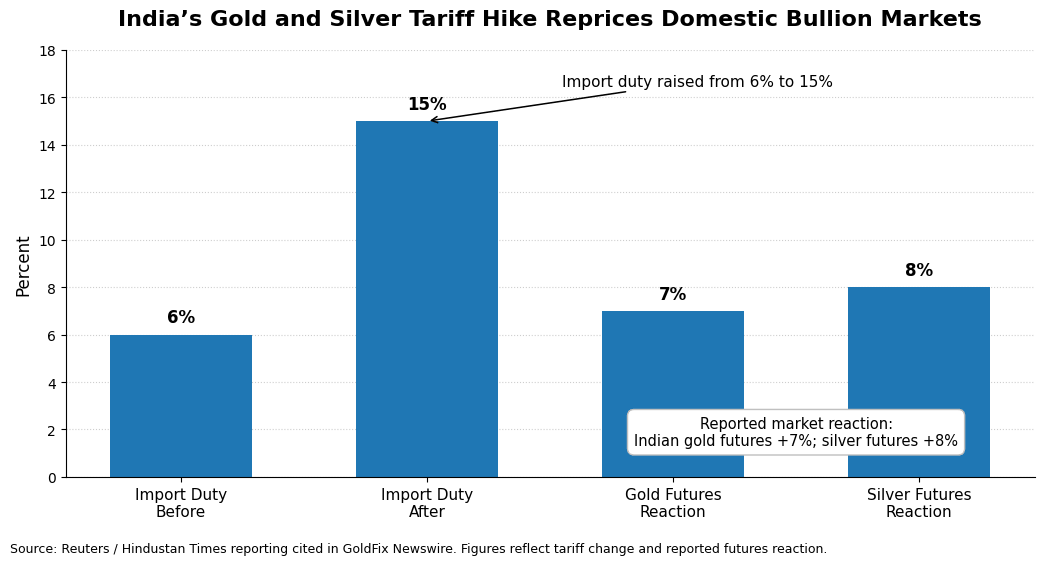

India sharply raised import taxes on gold and silver to 15% this week as Prime Minister Narendra Modi pushed for lower purchases of imported goods and greater focus on domestic economic stability.

Picture via Reuters: India typically buys between 700 and 900 metric tonnes of gold per year, making it either the world’s largest or second-largest gold consumer depending on the year and whether China is ahead.

The move raises tariffs on gold and silver from 6% to 15% and is being viewed as a direct attempt to slow the massive amount of precious metals flowing into the country. India is one of the world’s largest buyers of gold, and demand has remained extremely strong even as prices sit near record highs.

Modi recently urged citizens to “reduce use of foreign products,” tying the message to broader efforts aimed at reducing unnecessary imports and strengthening the local economy during a period of higher global energy costs and geopolitical uncertainty.

The market reaction was immediate. Indian gold futures jumped more than 7% after the announcement, while silver futures surged roughly 8% as traders priced in the higher cost of importing bullion into the country.

Analysts say the higher tariffs may reduce official imports over time, though some warn they could also increase unofficial channels and smuggling activity, similar to what happened during earlier periods of high import taxes.

The bigger story, however, is the scale of demand itself. Despite rising prices and now significantly higher taxes, Indian demand for gold and silver continues to surge. That suggests many consumers increasingly view precious metals as long-term stores of value and financial protection, especially during periods of global uncertainty and rising economic stress.