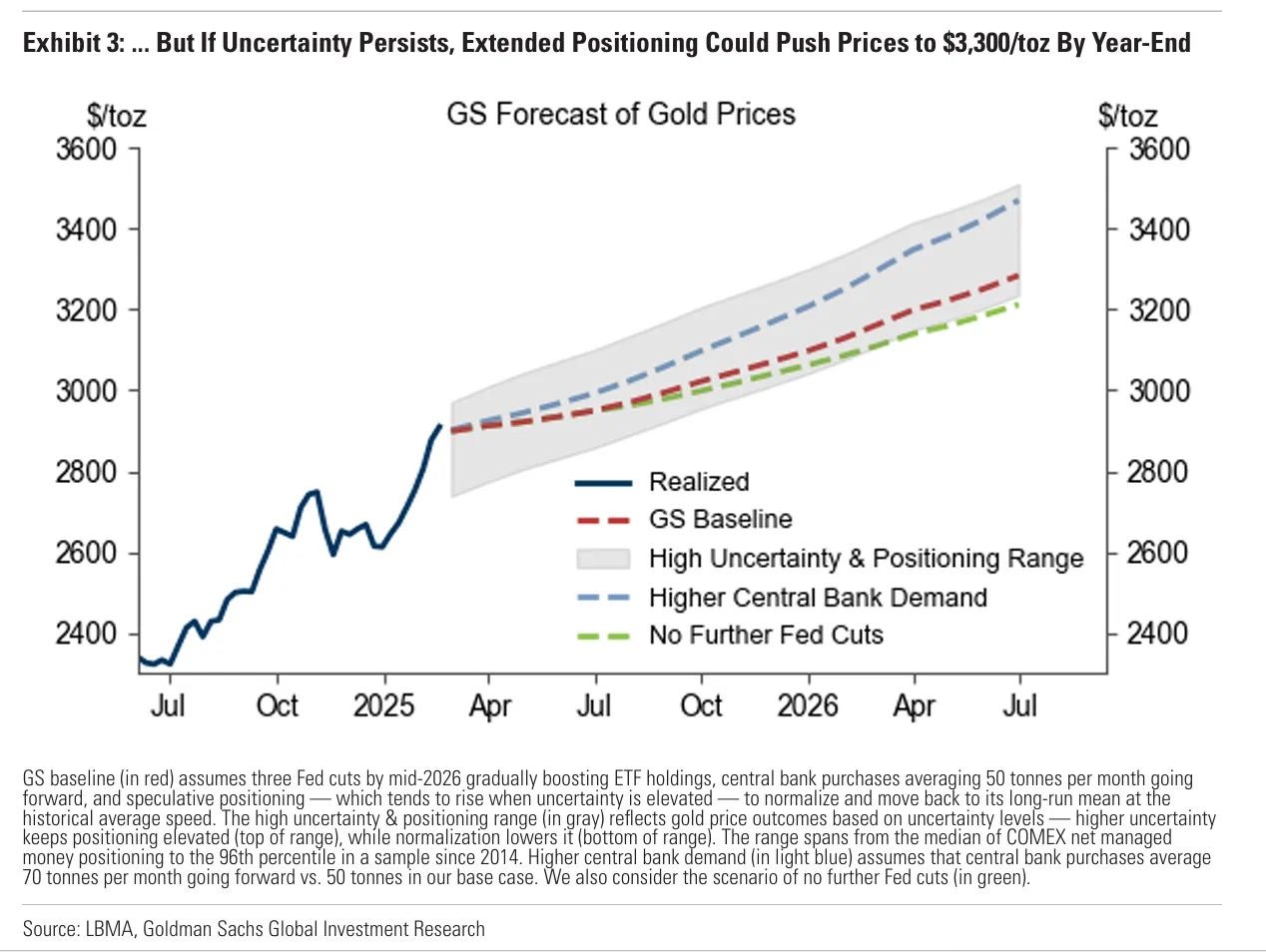

Goldman Sachs raised its gold price forecast for the end of 2025 to $3,100 per ounce, up from its previous estimate of $2,890. The adjustment reflects the bank’s expectation of sustained central bank physical demand driving the market higher.

While base case expectations are for $3,100/oz, the bank highlights further upside potential, including policy uncertainty and fiscal sustainability concerns, which could push gold to $3,300/oz or higher by year-end.

Before we drill down on this report, some context is in order, namely a bigger picture overview of the London Gold drainage situation, a signpost of why we feel Goldman’s target is low.

Central Bank Demand Rises Again

Goldman estimates that a “structural rise in central bank demand would add 9% to gold prices by the end of 2025.” The bank increased its central bank demand assumption to 50 tonnes per month, up from 41 tonnes. Should monthly purchases average 70 tonnes, Goldman sees gold reaching $3,300 per ounce by year-end 2025.

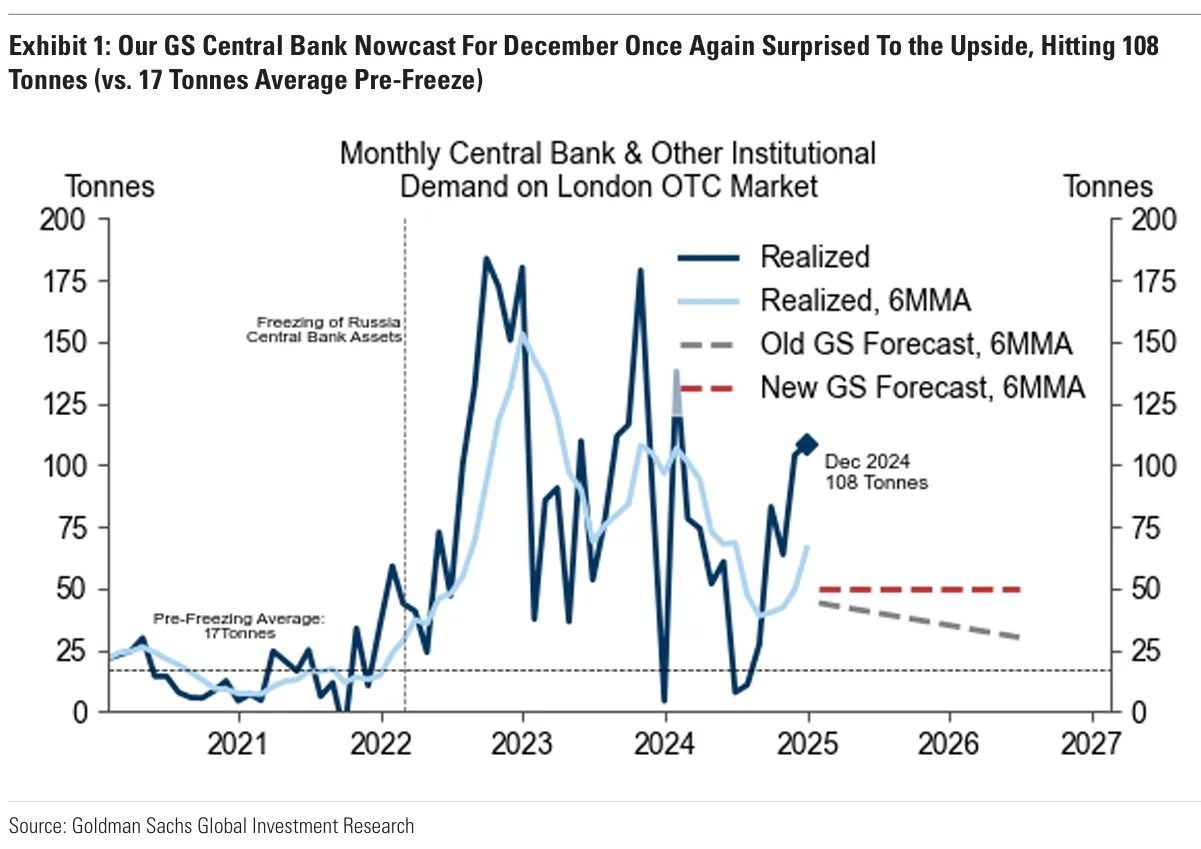

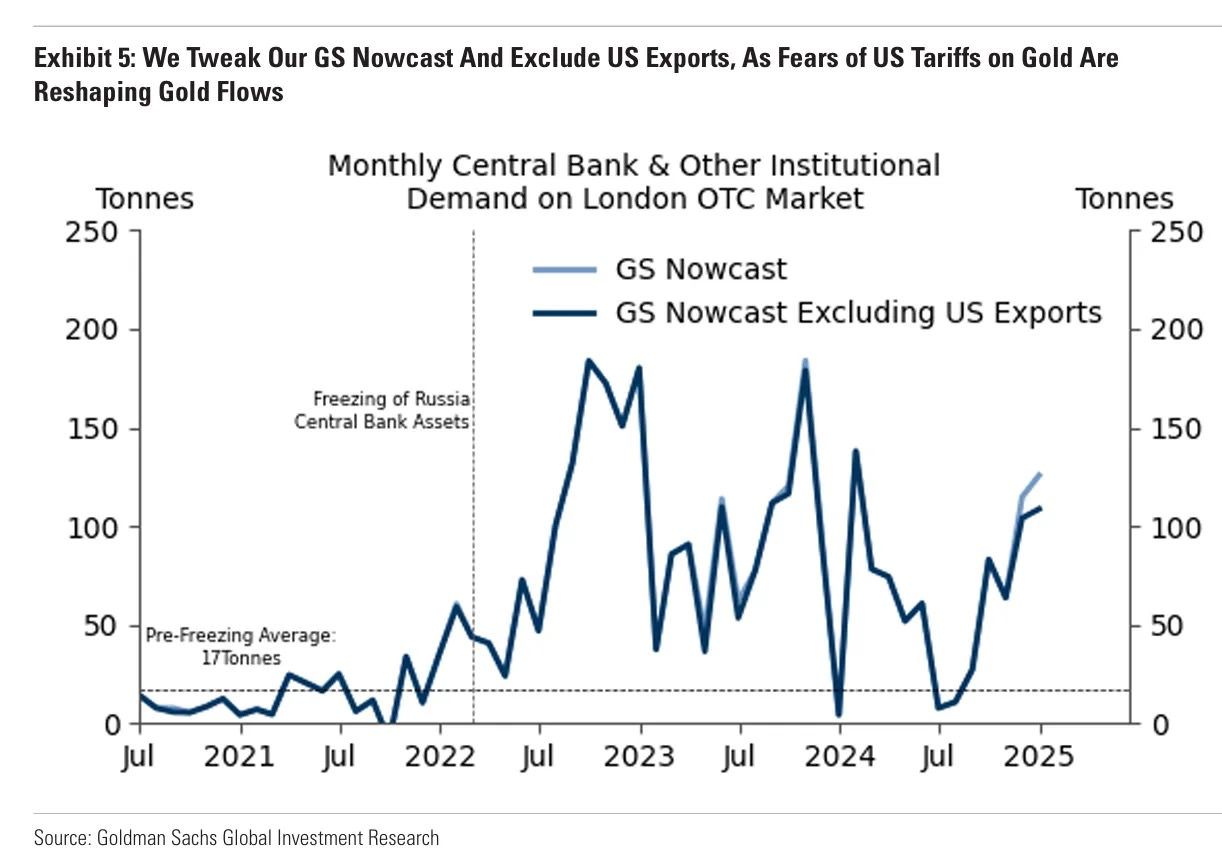

“The December reading of our GS nowcast of central bank and other institutional gold demand on the London OTC market came in strong at 108 tonnes… China was again the largest buyer, adding 45 tonnes.” – Goldman Sachs.

As a result, Goldman raised its baseline assumption for central bank buying to 50 tonnes per month (from 41 tonnes). This sustained demand is expected to add 9% to gold prices by the end of 2025.

We would add, the change from 41 to 50 tonnes is even more significant when you consider the bank changed a 6 month moving average after 2 months of data— not a one month data point— by over 20%.

Additionally, it is notable the Goldman report targets did not consider the recent changes in China’s capital structure. Bank of America factors in that China has just begun permitting its insurers to offer Gold-based investments to clients, 70 tonnes is actually conservative according to Bank of America.

The Path to $3,500 Goes Through China Insurers

Bank of America expects that China’s insurance companies will purchase gold actively and use their allowance within a year. Putting concrete numbers behind this, the purchases could generate around 300 tonnes of gold purchases.

If you are old enough to remember, this is very similar to what Ronald Reagan did in the 1980s when he deregulated insurance companies enabling them to invest in and offer more stock-based insurance products. This was one harbinger of the great 1980s bull market.

China, by enabling insurance companies to offer Gold to clients, is doing the same thing, but for Gold and Silver.

Taken together, the probability of Goldman’s $3,300 target, and even BOA’s $3,500 target are not insignificant. Goldman also notes significant upside risks not yet in their price calculus. We make it clear that one of them, the Tariff risk, is already manifesting and will not stop.

More Upside Surprise Risks

Goldman outlined multiple scenarios for gold’s trajectory:

– If the Fed does not cut for the rest of 2025, even with no further increases in China buying, gold is forecasted to hit $3,060 per ounce – green line

– If ETF inflows pick up alongside rate cuts as forecast, gold could reach $3,100 – red line

They argue that if policy uncertainty, including tariffs, intensifies, long-term speculative positioning could drive prices to $3,300 per ounce.

The Kicker: Tariffs are Outrageously Bullish Gold

To put a fine point on it: Policy uncertainty is already intensifying. Gold is a hedge against uncertainty, as most know. But what happens when that uncertainty actually resolves negatively? The graphic below says what happens. More Gold is bought, and less Gold is exported freely.

“We Tweak Our GS Nowcast (OTC London Bullion monitor) and Exclude US Exports, As Fears of Tariffs on Gold Are Reshaping Gold Flows” – Goldman Sachs

If the US puts tariffs on Gold, it must also cease exporting its own gold. It must protect what gold it has since the US have effectively cut off its own suppliers.

With this in mind, what happens to Silver if we tariff monetary metals. The US is much more dependent on Silver imports for replenishment than Gold. You cannot responsibly tariff what you need to buy!

Here’s the kicker. Tariffs are bullish for Gold even if they do not apply to Gold itself.

Why? Any nation tariffed by the USA—even without Gold and Silver tariffed—is one step closer to having that nation’s sovereign wealth confiscated by the US as was done to Russia in 2022. As a nation’s fear of eventual confiscation escalates, so does its desire to get out of held dollars and treasuries (euphemistically called “dollar-diversification”) and replace those with something that cannot be confiscated: Gold and Silver in hand. Specifically for Sovereign entities:

IF: Tariffs >> Sanctions >> Confiscation Risk

THEN: Sell Treasuries >> Buy Gold and Silver

The risk of confiscation starting with tariffs in a post 2022 Russian-Sanction world is very clear. You cannot own just dollars.

Goldman’s Target is Low

Goldman reiterated its “buy gold” trading stance. The bank emphasized gold’s value as a hedge against risks such as trade tensions, potential Fed policy missteps, and recession threats, noting these could push gold toward the upper end of its uncertainty range.

Given that Goldman’s analysis does not factor in the Chinese insurance industry’s incipient physical off take, we think Goldman is holding back on their bullishness. The higher upside is all but certain if China’s insurance industry buys in.